The UK abolished the long-standing non-domicile regime on 6 April 2025. The remittance basis was replaced by a 4-year Foreign Income and Gains (FIG) exemption available only to new UK residents who have not been UK-resident for the prior ten tax years. Long-resident UK non-doms now face worldwide income and gains taxation as it arises. Time-limited transitional reliefs exist including a Temporary Repatriation Facility (TRF) but the broad direction is clear and the window to plan is finite. For individuals considering their next steps, exploring Cyprus relocation services may form part of a broader relocation strategy.

What changed on 6 April 2025

The Finance Act 2025 ended the remittance basis of taxation for UK-resident non-domiciliaries. For decades, the regime allowed long-term UK residents who were not UK-domiciled to keep offshore income and gains outside the UK tax net, provided those funds were not remitted to the UK. The change moves the UK to a residence-based system aligned with the international norm.

From 6 April 2025, UK tax residents are taxed on their worldwide income and gains as they arise, regardless of whether the funds are brought into the UK. The only meaningful exemption is the new FIG regime, which is available only to new arrivals not to existing long-term UK non-doms.

The 4-year FIG regime-who qualifies

The Foreign Income and Gains regime is a four-year exemption available to individuals who become UK tax resident from 6 April 2025 onwards, provided they have not been UK tax resident in any of the prior ten tax years. During the four-year window, qualifying foreign income and gains are exempt from UK tax even if remitted to the UK.

The FIG regime applies for the year of arrival and the subsequent three tax years a strict four-year clock. After year four, the individual becomes subject to standard worldwide taxation on the same basis as any other UK resident. The regime cannot be re-claimed by leaving and returning.

Important: the FIG regime offers no relief for individuals who were UK-resident at any point in the prior ten tax years. For most long-resident UK non-doms, this means there is no equivalent ongoing exemption.

Transitional reliefs – the Temporary Repatriation Facility

Recognising that the abolition would otherwise lock out years of accumulated offshore funds, the legislation introduced the Temporary Repatriation Facility (TRF). The TRF allows individuals who previously claimed the remittance basis to bring historic foreign income and gains into the UK at reduced rates.

TRF rates are 12% for the 2025/26 and 2026/27 tax years, rising to 15% for 2027/28. After 5 April 2028, the TRF closes and any pre-2025 untaxed offshore funds remain subject to standard remittance taxation if brought into the UK in future. The TRF is a one-off window, not a permanent feature.

Other transitional features include rebasing relief for certain foreign assets and a temporary 50% reduction in foreign income subject to tax in 2025/26 for individuals already non-domiciled at 5 April 2025 both narrow and time-limited.

What this means for long-resident UK non-doms

If you have been a UK resident non-dom for several years, the 4-year FIG regime does not apply to you. From 6 April 2025, your offshore income and gains are taxable in the UK as they arise. Trust distributions, foreign dividends, foreign capital gains, foreign rental income all now sit in the UK tax net at standard rates.

The TRF gives you a window to bring historic untaxed offshore funds into the UK at 12–15% meaningfully below the standard rates that would otherwise apply on remittance. For many long-resident non-doms, deciding whether to use the TRF (and at what scale) is the single most consequential tax decision of the next two years.

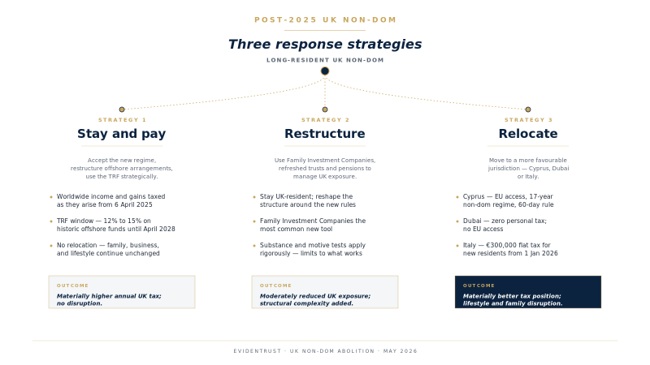

Three response strategies

Long-resident UK non-doms are taking one of three approaches. None is universally right the choice depends on family situation, business interests, lifestyle priorities, and risk appetite.

Strategy 1: Stay and pay

Accept the new regime, restructure offshore arrangements to manage UK exposure, use the TRF strategically to repatriate funds at reduced rates, and continue to live in the UK. This is the right answer where family ties, business operations or lifestyle preferences make relocation impractical. The cost is materially higher annual UK tax.

Strategy 2: Restructure without moving

Use Family Investment Companies (FICs), pension structures, or refreshed trust arrangements to manage the UK tax footprint while remaining UK resident. This approach has become more popular since April 2025 but has limits most offshore structures no longer produce the outcomes they did under the remittance basis, and substance and motive tests apply rigorously.

Strategy 3: Relocate

Move to a jurisdiction that offers a more favourable tax position. The three jurisdictions taking the most UK relocators in 2025–2026 are Cyprus, Dubai and Italy. Cyprus (EU, English-speaking, 17-year non-dom regime), Dubai (no personal income tax, no EU access), and Italy (€300,000 annual flat tax for new residents from 1 January 2026, doubled from €200k).

Why Cyprus has emerged as the most common destination

Cyprus has become one of the most credible relocation destinations for UK-origin non-doms for four practical reasons.

First, Cyprus offers a Cyprus non-domicile regime that exempts worldwide dividends, interest and rental income from Special Defence Contribution for 17 years the longest such window remaining in the EU. Second, Cyprus simplified its 60-day tax residency rule on 1 January 2026, allowing dual residency to be resolved under tie-breaker treaty rules rather than requiring a clean break from another country. Third, Cyprus operates entirely in English at professional services level, with a well-developed banking, legal and accounting sector. Fourth, Cyprus remains in the EU, providing freedom of movement, family-friendly schooling, and ongoing access to the European single market.

The Cyprus 15% corporate tax rate came into effect from 1 January 2026 (up from 12.5%) to align with the OECD Pillar Two minimum framework. Even at 15%, combined with the IP Box (giving an effective rate of around 2.5% on qualifying IP income), Cyprus remains one of the most competitive jurisdictions in the EU for individuals with corporate income.

Practical action points

- Quantify your post-April 2025 UK tax position. Project your worldwide income and gains as they will be taxed under the new regime most long-resident non-doms underestimate the change.

- Model the Temporary Repatriation Facility against your historic offshore funds. The 12–15% rates expire in April 2028, the window is finite and the decision is time-sensitive.

- Decide which of the three response strategies fits your situation, ideally before the start of the 2026/27 UK tax year (6 April 2026).

- If relocation is on the table, narrow the destination shortlist by tax outcome, EU access, family considerations, and lifestyle. Most UK relocators end up choosing between Cyprus, Dubai and Italy.

- Engage a qualified destination-country adviser before committing the choice between destinations is rarely as clear-cut as headline tax rates suggest.

Frequently asked questions

Does the FIG regime apply to me if I have been UK-resident for years?

No. The 4-year FIG regime is only available to individuals who have not been UK tax resident in any of the prior ten tax years. Long-resident UK non-doms do not qualify and have no equivalent ongoing exemption.

What is the Temporary Repatriation Facility?

The TRF lets individuals who previously claimed the remittance basis bring historic offshore funds into the UK at reduced rates — 12% for tax years 2025/26 and 2026/27, rising to 15% for 2027/28. The facility closes after 5 April 2028.

Is Cyprus the only relocation option?

No. The three most common destinations for UK-origin non-doms are Cyprus, Dubai and Italy. Each has materially different propositions — Cyprus offers EU access plus a 17-year non-dom regime, Dubai offers zero personal income tax but no EU access, Italy offers a €300,000-per-year flat tax for HNWIs from 1 January 2026.

How quickly can I become a Cyprus tax resident?

Under the simplified 60-day rule, you can become a Cyprus tax resident with sixty days' presence, business activity in Cyprus, a permanent home, and no more than 183 days in any other single country. Tax residency registration and non-dom status filings typically take 3–6 weeks once you are in Cyprus.

Do I need to leave the UK before April 2026 to benefit from a move?

There is no specific deadline tied to the relocation itself — but the Temporary Repatriation Facility's reduced rates step up after 2026/27 and expire entirely in 2028. The earlier you plan, the more flexibility you have over which UK tax year your move falls into and how you sequence the use of the TRF.

Speak with Evidentrust

Evidentrust is a Cyprus-based, ICPAC-member accounting, audit, tax and advisory firm. We work with UK-origin individuals, families and business owners considering Cyprus as a post-April 2025 destination. The first conversation is short, without obligation, and is intended to help you decide whether Cyprus is the right fit for your situation. If you are considering Cyprus relocation services, our advisers can help you assess whether Cyprus is the right fit for your circumstances.