Cyprus Benefits in Kind

The Tax Department (“TD”) has published an Informative Guide which explains the tax treatment of certain benefits offered by employers to employees and persons who hold or are deemed to hold an office. The Informative Guide provides clear guidelines as to the proper valuation of the Cyprus Benefits in Kind, for the purpose of consistency, clarity and uniformity, clearing any ambiguities.

In addition, the TD issued Circular 32 and Circular 37 both of which provide additional information on the documentation to be held and how the benefits in kind are calculated.

The taxation of benefits is provided in Article 5 of the Income Tax Law, according to which benefits from any office or employment, provided to an employee or to a member of his family either in cash or otherwise, are subject to tax.

The guide describes how the TD intends to apply the law as from 1 January 2019. Nevertheless, the subject provisions may be applied for previous years as well.

Scope and categories

Benefit in Kind (“BIK”) is considered to be the benefit that is, or is deemed to be, granted in connection with any employment or the holding of an office.

The benefit can be in the form of cash or any other cash equivalent received under an employee – employer relationship, or by a connected person of the employer, or by third parties.

Scope

The benefits in kind apply to the below individuals:

- Employees:

- with or without contract

- part or full time

- existing or former

- Persons who hold or are deemed to hold an office

- Directors

- Individuals who exercise control

- Individuals with duties similar to the Directors’

In addition, when the benefit is granted to a member of the family or household of any of the above persons, then the benefit shall be deemed to be provided to that person.

Categories of benefits in kind (“BIK”)

- Benefits related to the use of cars

- Benefits related to accommodation and use of assets

- Other benefits

1. Benefits Related To the Use of Cars

A BIK related to the use of cars arises where there is a usual element of private use as defined below:

• The car is at the disposal of an individual, or;

• The car is used on non-working hours, or;

• The car is not kept at the premises of the employer during the night or the weekends, or;

• The car is used for private purposes;

The BIK does not arise to employees who are drivers, messengers, distributors or other persons, for whom the use of the car is necessary for the execution of their duties, provided that they use the car during working hours.

The three types of benefits in kind related to the use of cars are as follows

a. Use of cars

b. Use of commercial car (van)

c. Reimbursements for the use of private cars

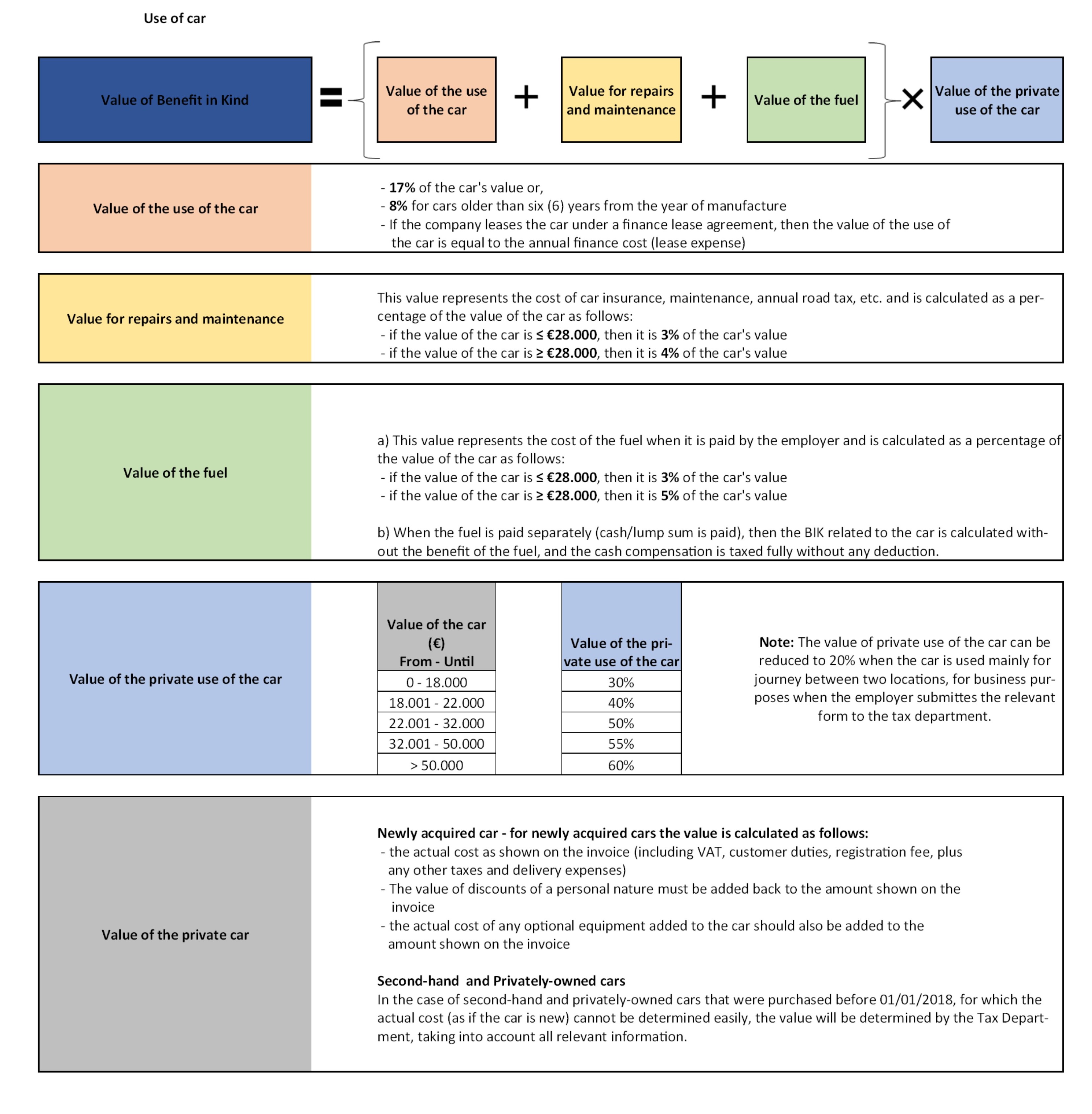

a. Use of Cars

A benefit in kind arises where there is a usual element of private use and its value is calculated as follows:

Reduced value of private use to 20%

To use the 20% rate for the calculation of BIK, employers are first required to complete the form Τ.Γ.286A which must be submitted and approved by the tax department.

b. Use of commercial car (van)

A benefit in kind arises when the following conditions are met:

c. Reimbursements for the use of private cars

The value of the benefit in kind is calculated as 50% of the annual compensation (up to €3.000) to employees in relation to the use of his/her own vehicle for business purposes, subject to the below conditions.

“kilometres travelled” basis

When the compensations are granted to the employee who uses his private car for business purposes on the basis of the distance travelled (with a maximum of 25 cents per kilometre), these repayments do not constitute a benefit in kind, on the provision that the employer keeps a log book for at least six years.

2. Benefits Related accommodation and use of assets

The provision of assets (e.g. accommodation, furniture, boats, machinery, etc.) to the employee when they belong to the employer and/or leased and/or rented by the employer, can be considered as benefits in kind.

The private use of the below assets, falls within the scope of benefits related to accommodation:

- Accommodation

- Furniture

- Boats

- Aircrafts

- Machinery

The Cyprus Benefits in Kind arises:

- On the date that the individual moves into the property, if the benefit is related to immovable property

- On the first day at which the asset is put to the disposal of the individual, if the benefit is related to assets other than immovable property

The annual value of the benefits in kind for the use of assets applies for as long as the asset is at the disposal of the beneficiary and is determined as follows:

3. Other Cyprus Benefits in Kind

Any other benefit in kind that does not fall within the above categories, is considered to fall into this category and includes:

In general, the value of the benefits in kind in this category is the market value (normal selling price less discounts provided to the general public) reduced by the price paid by the employee. However, the guidance issued by the Tax Authorities provides for specific treatment for the following cases:

| Cyprus Benefits in Kind | Explanations |

| Goods/Services which are produced/provided in the business course of the employer, provided to the employee | BIK is the difference between the market value of the goods/services, less any amount paid by the employee (subject to a conditional first €500 exemption) |

| Goods/Services which do not form part of the business of the employer or of a party related to the employer | BIK is the higher of: the market value of the good/service less any mount paid by the employee, or

The acquisition cost of the employer for the good/service less any amount paid by the employee |

| Provision of assets (tangible/intangible) | The value of the BIK depends on whether the asset “forms part of the business activity of the employer” or not. |

| Repayment of professional expenses: | BIK is the price that the employer paid plus any associated costs, subject to certain restrictions. |

| Business trips | No BIK arises provided that the daily amount paid is up to €250, or if the actual costs are paid.

A “per diem” payment in excess of the business trip expenses is considered to be BIK. If the trip is of excessive private purpose, the total amount of the business trip is considered to be BIK. |

| Meals | No BIK arises if the meals are provided to all employees or if the meals are provided in the course of a business event of the employer.

In all other cases the BIK is valued as the total cost of the employer. |

| Gifts | No BIK arises if: the gift does not exceed the amount of €300, and the employee only received one gift per year, and the employer does not claim the cost of the gift as an allowable deduction in his tax computation.

Performance related rewards are not considered to be BIK if the employer will not claim them al allowable deductions. |

| Costs related to the acquisition of tools | BIK equals to the cash provided for the acquisition of tools necessary for the executions of the employee’s duties. |

| Vacations, various presents and motive awards | BIK equals to the cost of the employer for vacations of the employee, his family or both.

Additionally, paid vacations/recreation expenses during a business trip are taxable BIK equal to the costs borne by the employer |

Exemptions relating to Cyprus Benefits in Kind

There are various cases where the employee receives a benefit which is not considered to be taxable as a BIK. It is important however to stress out that as a general principle, exemptions apply only to the extent where the payment or reimbursement to the employee is made against actual costs supported by payment receipts.

| Exemption – Cyprus Benefits in Kind | Description |

| Computer Equipment | Exempted, unless the employer is a provider of internet services, where the provision of free internet services and other free subscriptions is taxable |

| Telephone services | The payments / reimbursements made in respect of the use of telephones are exempted only if supported by the relevant payment receipts. However, limp sum cash payments are taxable. |

| Childcare facilities | Exempted, if the childcare services provided by the employer are with the workplace. |

| Goods cosumed in the workplace | Exempted, if the goods and services are manufactured / produced / provided by the employer or/and a connected company. |

| Newspapers | Exempted, if the subscriptions to newspapers or/and magazines or/and websites are related to the activities of the employer. |

| Awards for long term services | Exempted, if the award does not exceed the maximum amount of €100 per year of services, and no any similar award was given to the receiver in the last 10 years. |

| Subscriptions to professional bodies | Exempted, if the professional capacity of the employee is considered to be necessary for the execution of his duties, and for the benefit of the employer. |

| Christmas parties and events | Exempted, provided that the cost of the event per employee is reasonable |

| Uniforms and specialised attire | Exempted, when necessary for the execution of his duties. Any payments made by the employer related to the cleaning of the uniforms, are also not taxable. |

| Transportation to the workplace | Exempted, if the employer provides specific vehicles for the transportation of the employees, from specific gathering points, to the workplace. |

| Recreation areas | Exempted, if allowed to all employees, The payment for a club membership subscription is not taxable, if the membership is for the benefit of the employer and not the employee. |

| Relocation expenses | For the employee and his family. The exemption is the lump sum of €9.000 or the amount of the actual expenses incurred, if these are supported by the relevant invoices. |

| Training Courses/scholarships to employees | Exempted if the courses are necessary for the execution of the duties of the employee, and the expenses include only the course fees and the cost of the necessary books and materials, Taxable BIK only arises, if the main purpose of the training is for the benefit of the employee. |

Other information relating to the Cyprus Benefits in Kind

Keeping records

Employers are required to keep records indicating how the value of the benefits in kind has been determined and such records should be available for inspection when requested by the Tax Department.

The benefits in kind should be separated according to their category as defined in the informative guide. The form (Τ.Φ. 286Φ) presents the status to be retained, detailing what information should be retained in the employers’ records related to this subject and the information required to be documented with the appropriate supporting documentation. This particular form should be maintained for each person individually receiving a BIK.

Deductible expense

Since benefits in kind are taxed in the same way as salaries, the employer who will bear the cost of providing them will be able to deduct such cost from his taxable income under the same conditions that it would be deducted had it been a salary payment.

Employers’ registration and obligation to pay the relevant tax

Any person providing “benefits in kind” to an employee and any company or corporation providing benefits to its officers, even in cases where it does not have employees, is considered as an employer by the Tax Department and should register on the Employers’ Register and receive a T.I.C, which will enable the submission of the Employer’s Return (T.D. 7). The value of benefits in kind is taxed in the same way as the gross earnings, through the submission of the Form T.D. 7. Employers are required to declare the benefits in kind provided by them or by their connected companies.

Visit the MyCyprusTax for more information on how to submit you income tax form.

Visit the Cyprus Tax Department for more information on how to calculate your taxes.