2nd Provisional Tax / Temporary Tax 2020

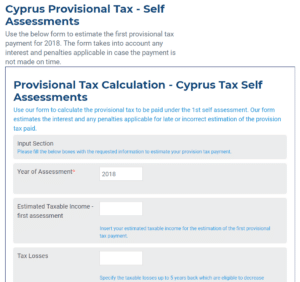

Cyprus Provisional Tax Calculation

2nd Self Assessment 2020

Using our calculator

Use our 2nd temporary tax calculator to estimate the 2nd provisional tax payment for 2020.

The calculator takes into account the chargeable income for the year, losses from previous year and any interest & penalties applicable in case the payment is not made on time. In addition, if the taxable income was revised under the 2nd tax assessment, then the form will also calculate any interest which is applicable on the portion of tax which should have been paid under the 1st assessment.

Annual Levy abolished from 2024 onwards

Annual Levy abolished from 2024 onwards The Department of Registrar [...]

Cyprus Tax Calendar 2024

Cyprus Tax Calendar 2024 Download or Subscribe to your Outlook [...]

Deemed Dividend Distribution for 2023

Deemed Dividend Distribution for 2023 Deadline 31/01/2024 Cyprus [...]

Revised Social Insurance Contribution Rates Starting 1st January 2024

Revised Social Insurance Contribution Rates Starting 1st January 2024 Author: Kyriacos [...]

Annual Levy abolished from 2024 onwards

Annual Levy abolished from 2024 onwards The Department of Registrar [...]

Cyprus Tax Calendar 2024

Cyprus Tax Calendar 2024 Download or Subscribe to your Outlook [...]

Deemed Dividend Distribution for 2023

Deemed Dividend Distribution for 2023 Deadline 31/01/2024 Cyprus [...]